-

The Alternate Data Flywheel: How Every Transaction Makes Lending Smarter

Fintechs use alternate data to reveal that consistent digital transactions lead to better repayment discipline, transforming lending models into self-learning systems.

-

How Real-Time Alternate Data is Powering Sub-30-day Lending

Introduction India’s next wave of credit growth is not being written in 5-year tenures and large-ticket EMIs. It is being written in 7-day, 15-day and 30-day borrowing cycles with tiny tickets, fast decisions, and even faster repayments. A recent report from the Fintech Association for Consumer Empowerment (FACE) notes that digital lenders disbursed ₹97,381 crore…

-

Algorithmic Bias, Inclusion & Fairness in Alternate Data Lending

As India’s lending shifts towards machine-driven credit decisioning using alternate data, the potential for algorithmic bias emerges, posing risks to financial inclusion amidst regulatory expectations

-

How Digital Payments and Online Shopping Behaviours Are Shaping the Future of Credit Scoring

India’s lending landscape is evolving, with alternative data from e-commerce and digital payments offering deeper insights into borrowers, enhancing credit assessment and expanding financial inclusion.

-

The Data Dividend: How Alternate Data Can Create a $1 Trillion Credit Economy

India’s credit economy faces a transformation driven by alternate data, potentially unlocking $1 trillion in credit by 2030 for underserved borrowers and MSMEs.

-

Inside the SME Files: How GST, Trade Data, and MCA Filings Reveal Business Health

The SME Credit Visibility Gap: Why Traditional Models No Longer Suffice In 2024, a mid-sized auto components manufacturer in Coimbatore defaulted on a ₹60-lakh working capital loan. On paper, the business appeared sound as the audited statements were current, collateral was sufficient, and the bureau record was clear. Yet, beneath the surface, early indicators of…

-

The Gig Economy’s Hidden Credit Trail: Digital Footprints, Fraud & Risk in India

Imagine a delivery partner for Swiggy, who we shall call Anita, who earns ₹38,000 monthly via food-delivery assignments and banks every payout. On paper, she ticks the “stable income” box. But in the past 90 days Anita’s account shows multiple small credits, near-zero balance cycles within days of each payout, and several loan applications submitted…

-

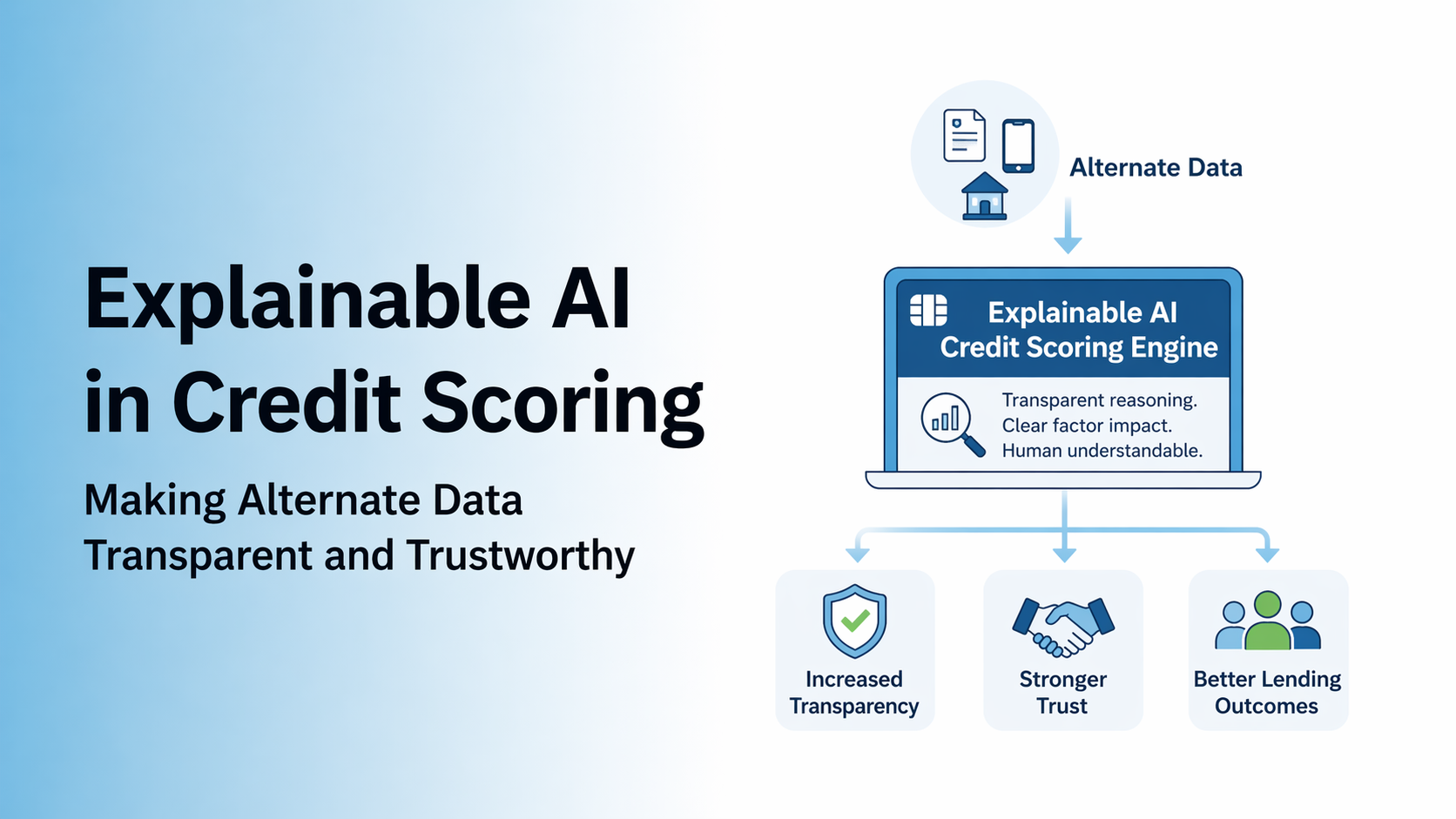

Explainable AI in Credit Scoring: Making Alternate Data Transparent and Trustworthy

A recent study reveals that 80% of AI projects in financial services fail due to a lack of trust and explainability. In India, explainable AI is crucial for transparent decision-making in lending, fostering trust and regulatory compliance.

-

Unlocking MSME & First-Time Borrower Credit with Alternate Data

The MSME Credit Assessment Challenge highlights how traditional financial documents fail to capture the true financial health of businesses, creating a visibility gap for lenders. Utilizing alternate data enhances underwriting accuracy and identifies potential credit stress early.

-

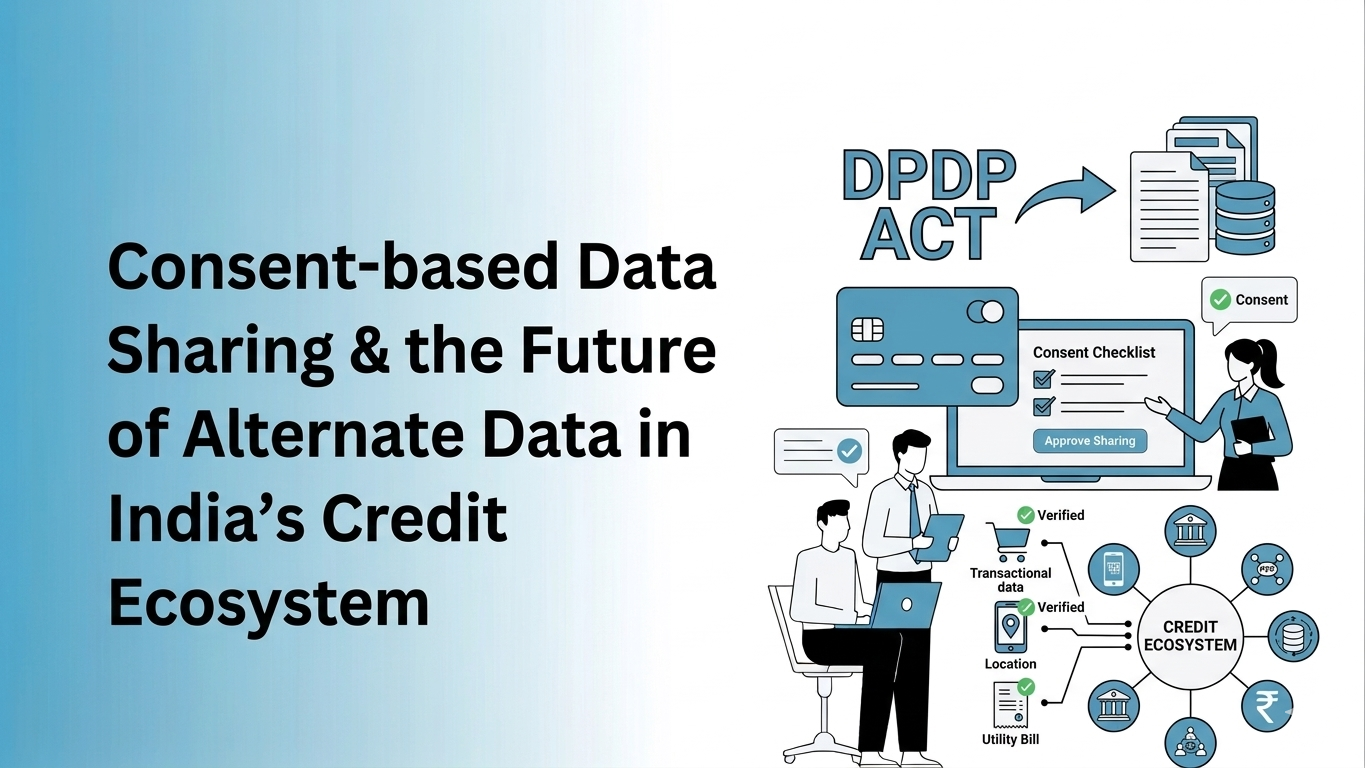

Consent-based Data Sharing & the Future of Alternate Data in India’s Credit Ecosystem

India’s financial data architecture is transforming with over 1.1 billion bank accounts enabled for secure data sharing via AA. This shift towards consent-based data sharing enhances accuracy in credit assessments and promotes financial inclusion!

-

How WhatsApp is Reshaping Lending in India

India’s lending industry faces challenges with high borrower drop-off rates despite technological advancements. WhatsApp offers a solution through real-time engagement, automation, and personalized communication, improving borrower satisfaction and conversion rates.

-

How Alternate Data Improves MSME Credit Underwriting?

MSME lending often suffers from limited visibility into real business performance. Learn how alternate data from bank transactions, GST filings, and digital payment trails helps lenders detect early stress, improve underwriting precision, and reduce NPAs.